While many countries struggle to tame inflation, Thailand has been facing deflationary pressures. This isn’t the first time Thailand has faced deflation: The last one was in late 2023 and early 2024, and before that, during the pandemic. So, what is going on now in the land of smiles?

At first glance, the lagging economic data don’t show alarm bells ringing: Retail sales (see here and here) grow at a steady pace, and unemployment is still below 1%. However, GDP growth is projected to reach 2% this year – in 2024 it was 2.4% – a bit slower pace; in addition, consumer confidence is at its lowest in over two years and the financial markets indicate some weakness: The SET index is down 20% YTD, and 10-year government bond yield has been falling, probably due to the Bank of Thailand’s (BOT) rate cuts and the deflationary pressures – suggesting flight to safety as the economy slows.

The March earthquake that was felt in Bangkok and the latest political turbulences didn’t help market sentiment, and then there is the weakness in tourism and the US trade war.

This year’s tourism hasn’t been good, with a decline of 7.5% in the number of tourists visiting the Kingdom in the first nine months of 2025, compared to 2024. Most of the decrease is from China, which accounted for a fifth of all tourists coming to Thailand.

Moreover, Trump has slapped tariffs on Thailand, as he did on many other countries; exports to the US market account for 20% of Thailand’s total. However, negotiations are still ongoing, so the actual extent of these tariffs on the economy remains unclear.

While these factors could have adversely affected consumers and markets, which, in turn, could have also affected inflation, a look at the components of the CPI reveals some insight behind this latest deflationary spell.

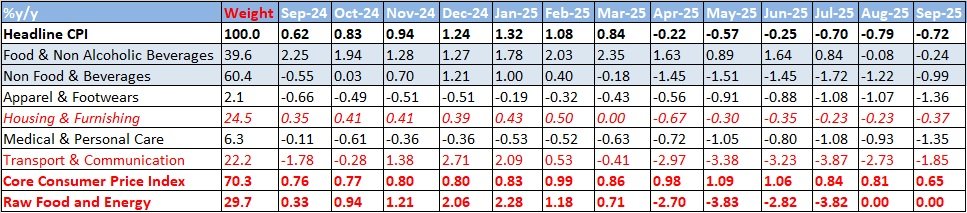

Breakdown of the components of the CPI

Housing & Furnishing and Transport & Communication, which, combined, account for 46.7% of the total basket of goods and services of the CPI, have been in negative territory in recent months.

Thailand’s CPI by main components

Source: CEIC, UOB Global Economics & Markets Research

However, according to the Bank of Thailand (BOT)’s MPC latest rate decision, the main reason for Thailand’s deflation is supply-side issues, citing falling prices in food and retail oil prices. While food and energy experienced a decline in prices in previous months, in August and September, their prices remained flat, even as prices related to Housing & Furnishing and Transport & Communication kept falling.

The table indicates that while Thailand’s deflation is related to supply-side issues in certain industries, it is driven by demand-side weakness stemming from the factors listed above.

Core inflation has been hovering slightly below 1% or close to it, which is at the lower end of the BOT’s 1-3% target. The current outlook by the BOT is that it will end the year at 0.9%.

From a policy standpoint, after excluding volatile food and energy prices, core inflation remains low. The BOT has already slashed rates by 75 bp this year and is expected to do so again at least once more. But even at the current rate of 1.5%, core inflation is still at a low end, and the rate cuts didn’t seem to raise it, for now.

All in all, the deflationary story is concentrated in specific sectors such as housing, transportation, energy, and food, driven by demand and supply-side issues. Even when excluding food and energy, inflation remains low and the BOT’s rate cuts haven’t put a dent so far in this deflationary story. After all, the BOT’s powers are limited, given that some of these issues, such as tariffs or political woes, aren’t easily fixed with lower interest rates.